Happy new year to you all,

2019 was a complicated though blisteringly high return year for most market indexes and thankfully my own book of assets. It was a very selective year though with 5 mega cap stocks in the US making much of the index gains.

It was another year where the base cyclical case didn’t play out exactly to plan. Again we needed to nibble and reactive to avoid losses and ensure we rode the gains. The projected C wave washout didn’t occur and instead we leap up to new highs as the secular bull market reversed the weakness and many asset prices soared higher once again. You had to roll with what price was telling us to survive and prosper.

So here we go on to another year. Lets hope its another good one.

Global Equities

Following a near 19 months of sideways trading in global equities and cyclical sectors in a bear market, the distributive top appeared in for global risk in H1 2019. Nonetheless by Q4 2019, with the US market at all-time highs and Europe breaking a 20-year resistances, the final push in global equities had commenced.

Here the 2020 markets projection:

The negation of the 2019 C wave sell off by central bank action, translated into fundamentals, has produced a “wave V” as a mini reflation cycle in a toppish Juglar Cycle in the US, whereas globally it´s just an economic rebound that makes the 2018 bear market a copy of 1998 on the way into a major top and subsequent synchronized Juglar Cycle decline/recession.

Bullish 2020 (presidential election year) but its a high conviction call that this “wave V” will be just a relatively short late cycle bull market lasting minimum into summer 2020 to more likely Q1 2021. In a wave V, we should expect, growing selectivity, deteriorating breadth/index momentum, and rising volatility.

Having said that, after 2019’s record ETF outflows of equities, there could well be selective surprises, where Europe is likely to be the outperformer candidate and where the breakout to a new 20-year high in the STOXX-600 is the trigger of a major squeeze higher.

Tactically, after impressive Q4 rally, markets are very overbought, with the high probability of a risk of a classic tactical washout from an mid January top into a later Q1 (March) bottom as the setup for a strong rally into summer. A potential summer top could be worst case the starting point of a volatile distributive top building process into Q1 2021 in the US, where stock picking and sector rotation should be key instead of chasing the SP500, which we see capped at 3600.

We expect performance to shift more into late cyclical (resource) sectors. We are bearish defensives where we see rising yields as a threat. Relatively our base case is that 2020 performance will be in order:

- Japan

- Asia/EM

- Europe

- US (US to strongly under perform in H2)

FX

After being structurally USD bullish since 2011, we have clear evidence that the 2018 wave 5 bull cycle in the DXY had topped. Tactically, after the Q4 2020 USD weakness, we expect a late Q1 USD rebound (versus high beta) as the setup for a wave 3 breakdown into summer and into Q1 2021.

We are bullish AUD, NZD, the Asian/EM block. We are bullish EUR and GBP.

Together with being bearish JPY, we see EURJPY as one of the key performers in 2020.

A USD bear market is the setup for a risk mkt regime shift on the macro side.

Commodities:

2020 is a bullish year for the commodity sector, where the 2011 secular bear market has based. After the 2018/2019 disinflation and subsequent reversal of this via central bank “actions” higher commodities and bullish copper as

leading indicator for a surprisingly strong comeback of inflation into 2020/2021 is the new high probability base case scenario.

Precious Metals

December 2015 was an 8-year cycle bottom in gold that is trading in a long-term bull market. After being bullish gold in 2019, we expect 2020 to be a trading year for gold. After a Q1 overshooting, we see gold vulnerable for a washout (rising yields) into summer/H2 before resuming its long-term bull market into 2021 and where silver will likely provide the +beta out performance to gold.

Asian/EM strong performance at this late cycle bull appears likely. With the bearish USD view, the MSCI

Emerging Market is likely in the early stages of a new cyclical bull market into H1 2021. Regional out performance by bullish China and Korea.

Japan has been trading sideways for nearly 2 years. With our bearish JPY view, we are bullish Nikkei-225, where we

expect a larger wave 5 to overshoot towards 30.000 into H1 2021.

Bonds:

The August low represents an early 4-year cycle global yield bottom where particularly the yield crash in Europe had all signs of a bubble top in bonds. Bonds are bearish in 2020, where after a tactical Q1 pullback, we should expect US 10-Year yields moving towards 2.6% – 2.8% into initially summer and ultimately into H1 2021.

Overall it would appear that we have the next piece in a potential structural comeback of inflation into this next decade, where at the end of the day, the likelihood is of moving into a stagflation rather than inflationary scenario. Rising inflation sooner or later kills every bull market (cyclical and secular bull markets). Analytically, this means that as long as we do not see a significant pickup in inflation we are in the sweet spot of a classic “goldilocks” scenario which is bullish risk. Having said this, if US equities are trading in a major new “wave V” and therefore moving into a secular peak, we should implicitly see very soon a significant rise of inflation, which is our main base case thesis for the next 2 years.

Summary

Despite the S&P-500 hitting new all-time highs in H2 2019, the 2018 long-term macro base case/cycle roadmap is unchanged albeit the timing is more complex. Particularly in the US, the current Juglar Cycle is extending where the length of the current economic expansion has reached record territory. However, the probability is that the

Juglar Cycle is mature/toppish and where a decline into a stag flationary recession is imminent, although the timing of the decline has obviously changed to the original 2018 scenario.

Cycle extension has also changed the larger Elliott Wave count. One consequence of this is, that we have to adjust our long-term Elliott Wave count in the S&P-500. Originally, we thought that the 2018 boom & bust cycle top was a major wave 5 top, and where our suggested early 2020 4-year cycle low projection and the subsequent bull cycle (accompanied by rising inflation) into the first half of the new decade, we would have already seen in the context of starting into a secular sideways trading range. Fact is, that with the US economic cycle extending, we are factually still in the old regime, so where we see the December 2018 S&P-500 low at 2347 as the bottom of a larger wave IV correction.

Conversely we can see for the MSCI World, the whole 2018 correction cycle has the structure of the favoured larger A-B-C correction cycle, in the S&P-500, wave IV was just a short and sharp correction. With that wave count, we see December 2018 as the formal starting point of a major wave V, which we think will complete the 2009 bull market in the first half of the new decade and which leaves our long-term cyclical model unchanged.

Concluding Words:

Our models and the recent price action sets the high probability base case which has not changed since last years projection that in the first half of this new decade we will see a generational turning point in financial markets, setting the trends for more than a decade into the 2030s.

Ill try and provide a part 2 to this summary release to drop down into regions and sectors and some individual picks. The concluding words shouldn’t surprise long term readers here and are ominous indeed. I will try and provide some additional words on these comments on the part2 post.

I will you all a very prosperous and happy and healthy 2020.

All the best

Rich

p.s. some comments here on gold and the important eurusd from Fitzpatrick at Citi

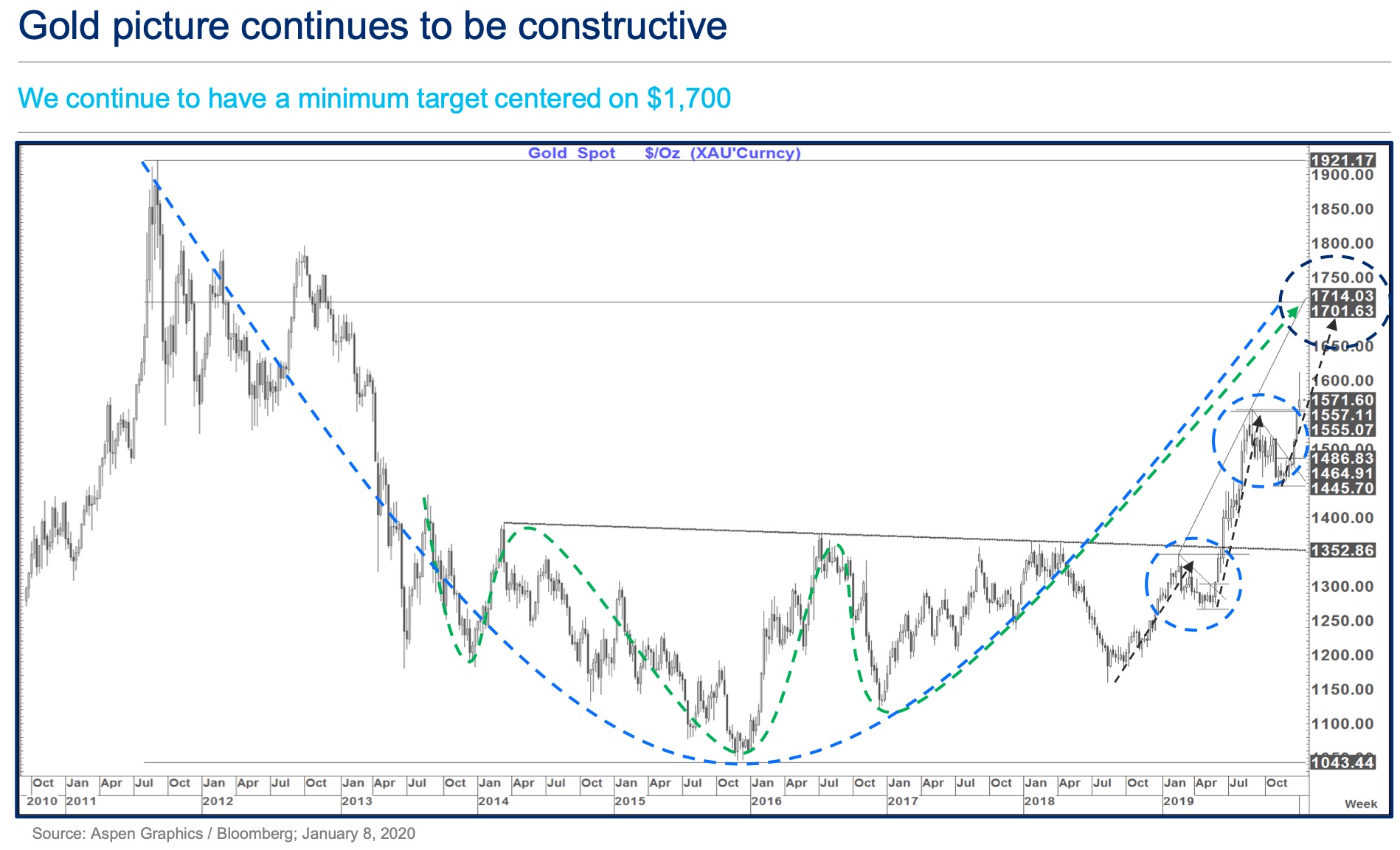

Top Citi Bank Technical Analyst Tom Fitzpatrick: Our bias remains for a move towards $1,700+ at a minimum with an argument to be made for a possible move to and maybe even above the all time highs.

Despite Pullbacks, $1,700+ Gold Is On The Way

We continue to hold the view that Gold can head to at least the $1,700+ area (possibly in Q1 2020).

This is both the target of the inverted head and shoulders and the 76.4% pullback of the fall from $1,921 to $1,043. The rising trend line off the Feb and Sept 2019 highs also converges with this area…

While the initial break higher this month was accompanied by elevated geopolitical risk the underlying picture looked bullish long before this development. This suggests that while some calm on that front might create a bit more choppiness near term they underlying bull trend remains intact.

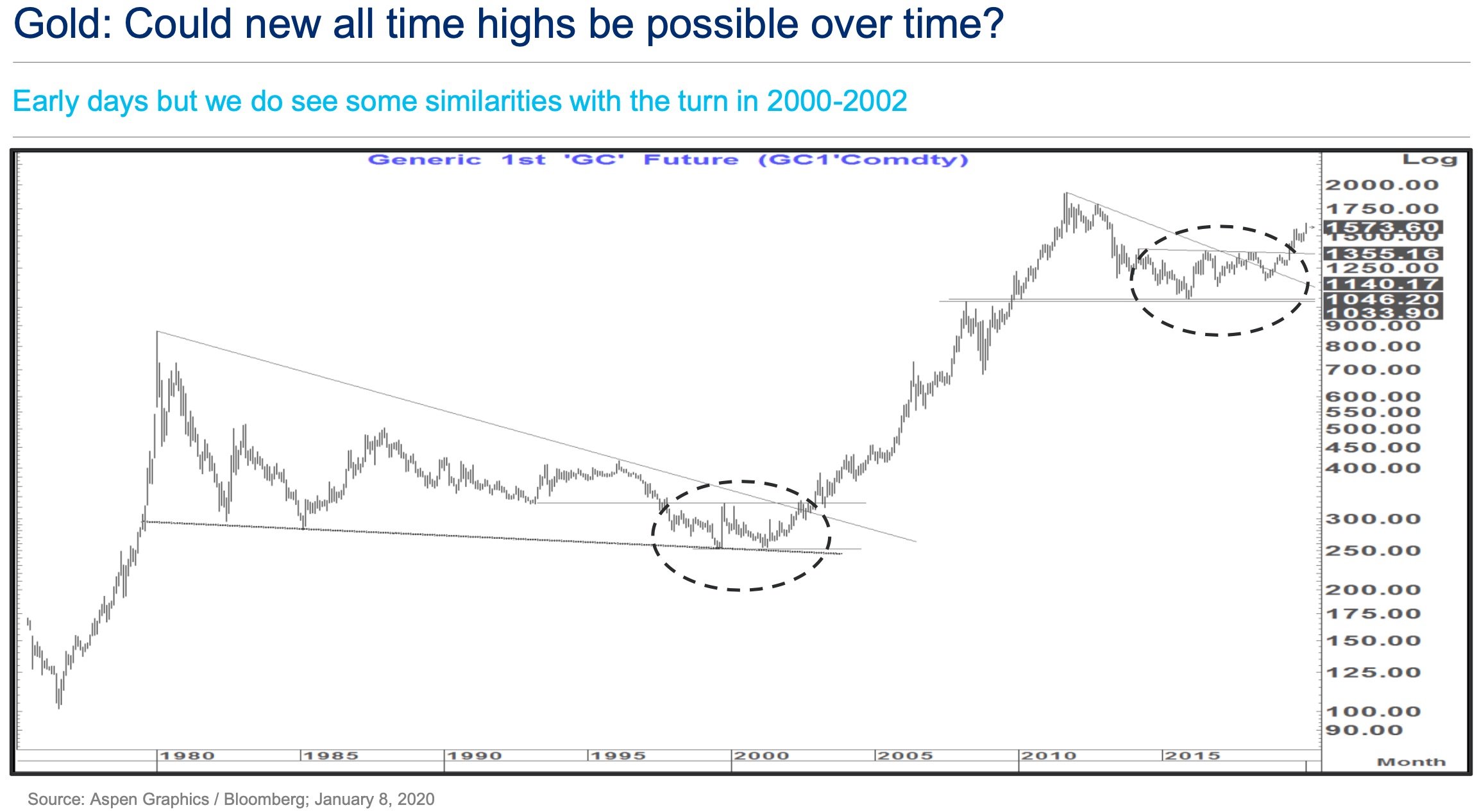

Gold Price May Hit New All-Time Highs

From a US economy/USD perspective we have been very focused on 2000-2002 (Not so much from an equity market perspective). That was a period that saw a trend low forming in Gold before a sharp turn higher.

Gold May Hit $2,100 This Year

Ultimately that resulted in a move to new all time highs (which required a much buffer percentage move that we would need today as the correction in 2011-2016 was much shorter in timeframe and shallower in magnitude than that seen in 1980-2000.) Even if we are on the page of the low to high bounce seen in 1985-1987 (Fitting more with our preferred Equity period where we are looking for a 15% up move in the S&P this year like that seen in 1986) it looks constructive for Gold. In 1986 Gold had a low to high move of 37% and an up year of 23%.

Similar numbers if seen this year could see Gold trade as high as $2,100 this year and potentially close the year as high as $1,870. 1986 was also a year of significant USD weakness.

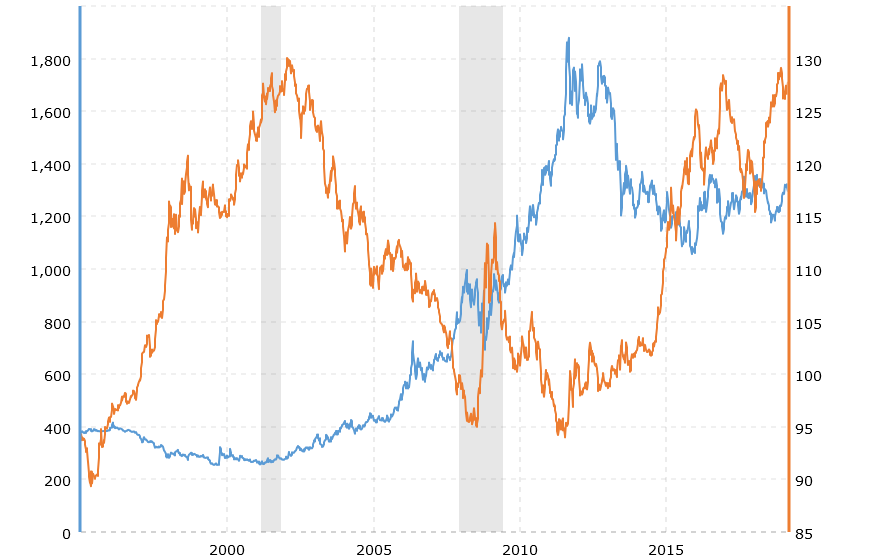

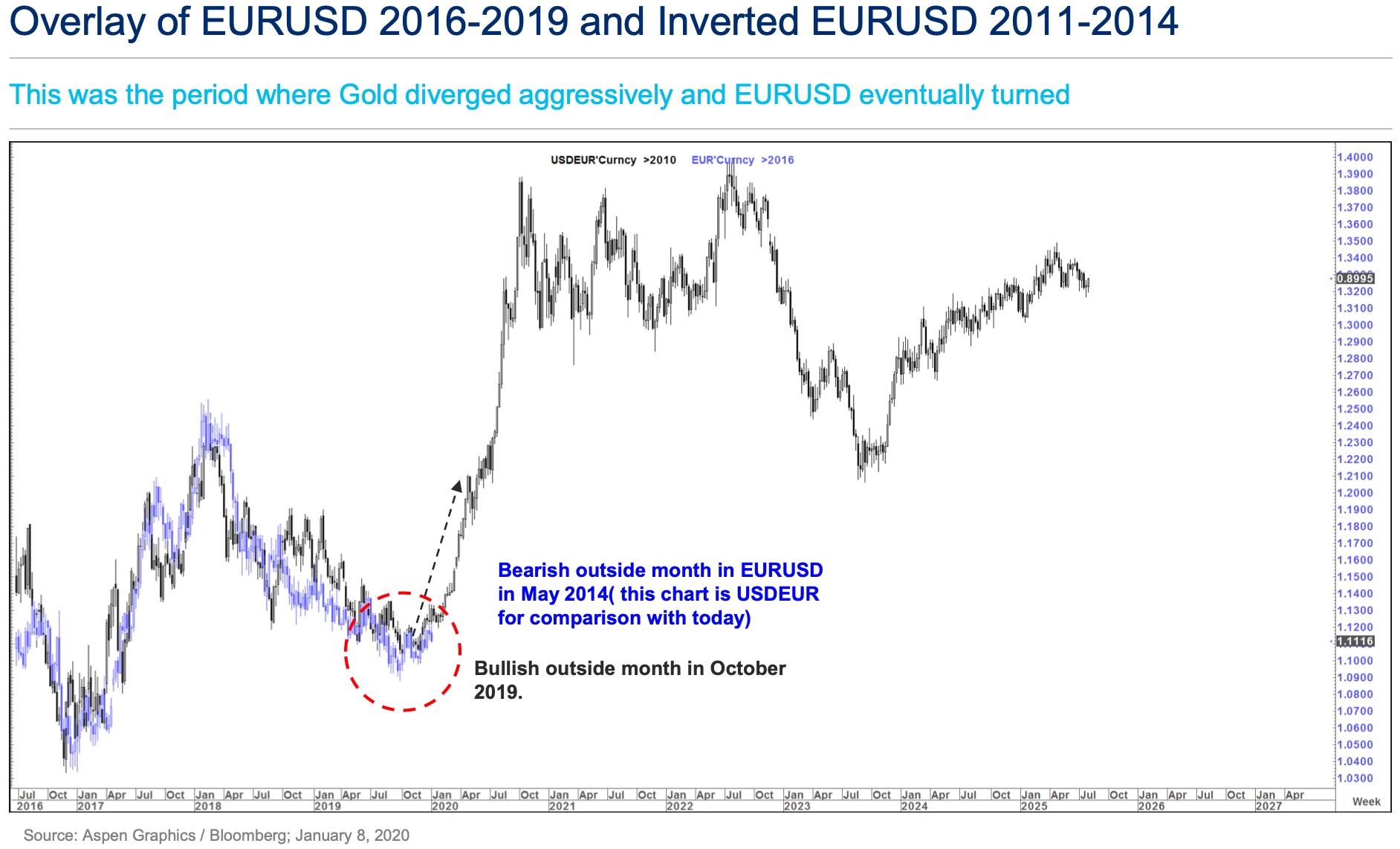

Since Gold peaked in 2011 there has (not surprisingly) been a close correlation to trending moves in Gold and in the USD (EURUSD used above).

Where those relationships broke down for a period- Gold has tended to ultimately give the correct signal.

That divergence is now the most severe since it happened in the other direction in 2012-2014 after which EURUSD fell sharply. The present pattern on EURUSD has been an almost perfect mirror image of that period.

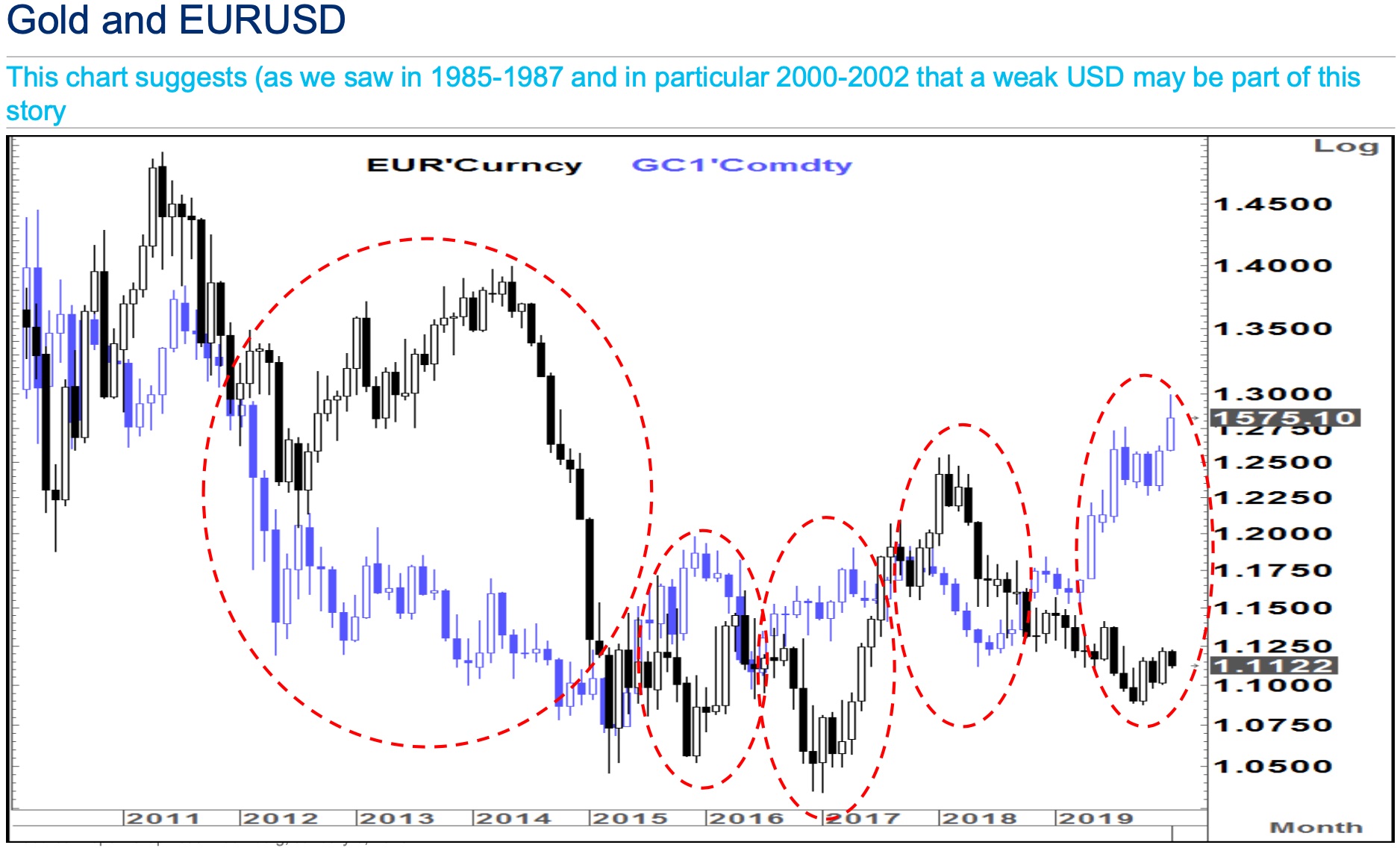

GOLD CATALYST: US Dollar Set To Plunge

The turn in EURUSD took place at the peak in May 2014 when it posted a bearish outside month. EURUSD posted a bullish outside month in October 2019.

As you can see price action continues to mirror that turn quite closely. It is worth noting that once EURUSD closed below the 55 week moving average in July 2014 it never looked back. The 55 week moving average (not shown) presently stands at 1.1196 and a weekly close above, if seen, would add to the bullish case.